Have you ever heard the word microfinance? Probably yes. Maybe you have heard some businessmen talking about it or your dad trying to teach you some economic concepts. In my case, I had heard my dad and brother discuss microfinance very often, but had always been afraid to even Google it because I thought it was a complicated concept. Due to the economics project I have been working on for the last couple of months, I have been indirectly learning about microfinance and, it turns out that it is not that complicated. Let me show you a little bit of what I’ve learned.

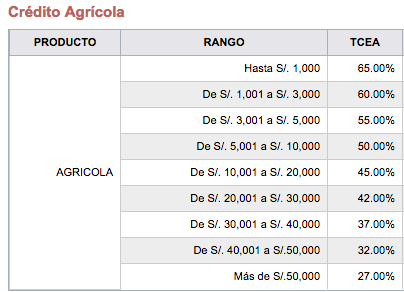

Before starting, what is microfinance exactly? It is the idea that people who receive a low income can get out of poverty if they have access to financial services. Banks which specialize in microfinance provide loans to low income people that normally do not have access to credit. They are normally smaller than normal banks and give out smaller loans. Traditional normal banks do not give out such small loans because the profit is too low, but microfinance banks have found a way to provide these loans. I was able to learn about microfinance one on one with people that are part of these banks and also the people on the other side, the ones that need these loans to get out of poverty. The first person I talked to was Vicente Montellanos, a farmer in Pachacamac. He was talking to me about his economic situation and how he needed to ask banks for loans because he couldn’t afford to buy a whole new production process. The main reason why he couldn’t afford it was because all of his crops were severely damaged, or didn’t grow completely, because of the El Nino phenomenon, which brings me to a main aspect of microfinance, risks. According to Robert Christen, microfinance specialist, and Henri Dommel, rural finance advisor, agriculture is widely considered more risky than any other industry. Weather, pests, diseases and other calamities affect the yield of crops, substantially in extreme cases. These risks are higher for farmers engaged in monoculture, which are more sensitive to the correct use of high-quality inputs or the timing of harvesting. In the case of Vicente, he was only planting onions and was tremendously affected by weather. Markets and prices are also risks associated with agriculture because many of these markets are informal. The prices that crops will sell for are unknown at the time of planting and vary depending on levels of production and the demand at the time of sale. Vicente was affected by these risks of markets and prices. He sold his products to an informal market that passed by Pachacamac once in awhile to buy as many crops as possible and the price that this informal market paid him was a very small amount compared to what he thought he would get. The reason why the price was very low was because the onions were not of high quality and therefore, Vicente lost a lot of money due to risks. These crop failures can greatly affect the farmers, since they invest all of their money in a crop that can easily be lost by all of these factors. So, it is not surprising that agricultural lending projects have poor repayment performance. For example, in 2003, Malawi’s crops failed to grow and this ended up affecting 176,000 families, leading them to poverty and severe hunger. (The Food and Agriculture Organization of the United Nations and the World Food Programme) Another person I talked to for this project was Rosanna Ramos Velita, the president of Caja Rural Los Andes, and she helped me understand the bank’s point of view on microfinance in Peru. Banks have a significant role in these people’s lives. They can change their economic situation by deciding if giving a loan or not. According to the International Finance Corporation, nearly 8 million people in rural areas of Peru remain under-served. Banks also have to understand the economic situation of the person when considering if giving a loan or not. An important factor they need to consider is the duration of the loan. As Ryan C. Fuhrmann said, “with a longer duration comes a higher risk that the loan will not be repaid. This is generally why long-term rates are higher than short-term ones.” This means that the higher the probability of customers not paying back, the higher the interest rate. Another factor they need to consider is the capacity of the customer to pay back a loan. This is done by looking at their incomes, their expenses and their properties. Another significant factor to consider are the risks, as Rosanna Ramos said, “As a financial entity, we can’t simply give credit to a product that we know might suffer a climatic risk, and we don’t want our client to go in debt and then not be able to pay their loans.” This is why, these banks also need to be aware of all the risks these farmers are exposed to because the risks can change quickly over time. For example, the conditions when you get the loan can be really different from the ones when you need to pay it back. One other factor that needs to be considered is the size of the loan. In Caja Rural for example, there is a 65% annual interest rate for borrowing 1,000 soles, whereas there is a 27% for borrowing more than 50,000 soles. The reason why interest rates decrease as the loan increases is because the cost for lending and collecting money in many small loans is higher than in fewer big loans, as mentioned by Richard Rosenberg, Scott Gaul, William Ford, and Olga Tomilova. In conclusion, microfinance is not an easy concept, especially because there are two sides to it. Farmers are one side of it and banks are the other. On one hand, farmers need the loans to produce their crops. Then on the other hand, it is extremely hard for banks to give loans to farmers because they are exposed to many uncontrollable risks that can leave them unable to pay back their loan. This results in a high interest rate for farmers who are the ones who lack the money but are also the ones that are producing crops.

0 Comments

Leave a Reply. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

March 2017

Categories |

RSS Feed

RSS Feed